The recent National Family Health Survey revealed that India has more females than males. Finally, India has embarked in a direction where girl children are embraced and empowered. However, Indian parents with a girl child have added responsibilities, especially marriage. LIC Kanyadan Policy is a scheme by the Life Insurance Corporation (LIC) of India to help girls’ parents fulfill their daughters’ financial needs.

Here’s all you need to know about LIC Kanyadan Policy, along with its features, benefits, and eligibility criteria.

Table of Contents

What Is LIC Kanyadan Policy?

LIC Kanyadan Policy is a new government scheme that helps parents secure a fund to support their daughters’ future needs. These primarily include education and marriage but may also comprise healthcare and other requirements. The scheme will be of great benefit to middle-class families who don’t have the resources to take care of their daughters’ basic needs and expenses.

The biggest expense for parents is their daughter’s marriage. The average middle-class wedding cost in India is Rs. 6-10 lakh, which can increase to Rs. 25-75 lakh in metropolitan cities. Many middle-class families don’t have the financial power to spend this magnitude of money on a single event. The Kanyadan Policy makes it easier.

In this scheme, a parent needs to pay a premium of Rs. 3,600 per month. After 25 years, they receive Rs. 27 lakhs. If you do the math, Rs. 3,600 per month for 25 years amounts to Rs. 10 lakh 80 thousand. Hence, you get more than double the amount you deposit. Besides, if the parent dies during the policy, the family won’t have to pay the premium, and they’ll receive Rs. 1 lakh per year from the government.

Also, please note that this policy is by the government of India, and hence, you can stay assured of the returns.

Features of LIC Kanyadan Policy

Now that we have looked at the basic overview of the Kanyadan Policy, let’s look at its features to help you get a detailed understanding of this scheme.

- Limited premium paying term, which is three years less than the policy payment term

- An option to make the payment monthly, quarterly, half-yearly, or annually

- 13 to 25 years of account maturity tenure

- Flexible policy plans of 6, 10, 15, and 20 years

- Get 10% of the assured sum every year till one year before the maturity date.

- Minimum five years of disability rider benefit for premium tenure

- The corporation will pay 80% of the premiums if the policyholder dies by suicide within 12 months of initiating the policy.

- The policyholder can apply for a loan if they pay a premium for three consecutive years.

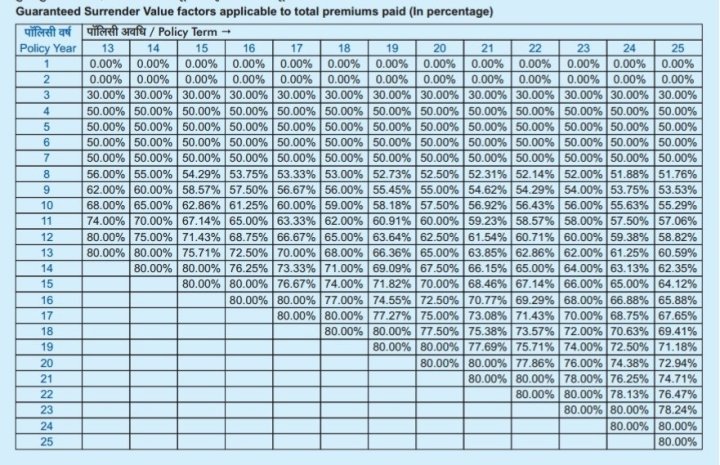

Note: Even though these features are picked from LIC’s resources and are 100% accurate, they are subject to changes. If you plan to buy this policy, visit your nearest LIC office and learn about all the features and specifications of this plan.

Advantages of LIC Kanyadan Policy

LIC Kanyadan Policy offers many benefits to parents. Let’s look at the key advantages of this policy and why you should buy it.

- Provide financial security to your daughter

- Get lump-sum payment on the maturity date

- No need to pay the premium if the policyholder dies

- Immediate compensation of Rs. 10 lakh if the policyholder dies by accident

- Immediate compensation of Rs. 5 lakh if the policyholder dies by natural or non-accidental cause

- Rs. 50,000 to Rs. 1 lakh compensation every year till maturity date if the policyholder dies

- Life risk cover till three years before maturity

- Get similar benefits to LIC Lakshya Policy

- Available for NRIs as well; no need to visit the country

Eligibility Criteria for LIC Kanyadan Policy

Having discussed the features and benefits of the policy, let’s look at its eligibility criteria. Look at these details to see if you are eligible.

- Minimum basic sum assured: Rs. 1 lakh

- Maximum basic sum assured: No limit

- Policy term: 13 years to 25 years

- Premium paying term: 3 years less than the policy term

- Minimum entry age: 18 years

- Maximum entry age: 50 years

- Maximum maturity age: 65 years

- Minimum age of daughter: 1 year

Please note that the eligibility criteria of policies are subject to change. Visit your nearest LIC office to get accurate information.

Income Tax Benefits of LIC Kanyadan Policy

Parents with a LIC Kanyadan Policy also get income tax benefits. According to the Income Tax Act 1961, any LIC policy premium is exempted from section 80C, with the maximum exemption being 1.5 lakh. Furthermore, policyholders don’t essentially need to deposit Rs. 121 every day. They can deposit more or less as per their requirements and spending power.

Should You Buy This Policy?

The ultimate question to answer is whether or not you should buy this policy. The benefits of this policy are clear. If you are a parent to a daughter and aren’t financially very capable, this policy can be a lifesaver for you. For an investment of Rs. 10.8 lakh, you get a return of 27 lakh — more than 100% return on investment.

However, you shouldn’t look at it as an investment scheme only. This policy helps you give a better life to your daughter. With education and marriage costs constantly increasing, financial planning is more important than ever. LIC Kanyadan Policy is a risk-free plan that lets you pay a small premium every month and get attractive returns on the maturity date.

Once the policy term ends, you get the entire amount (lump-sum) in your bank account. You can use the money to support your daughter’s marriage, higher education, or any other goal you want to achieve.

Conclusion

LIC Kanyadan Policy is a scheme by LIC to help parents empower their daughters with the needed financial resources. This scheme helps you pay a nominal monthly premium and get good returns on the maturity date. If you have a daughter who’s at least one year old, you should consider investing in this policy. By investing only Rs. 3,600 per month, you can get up to Rs. 27 lakh after 25 years.

So, what did you like and dislike about LIC Kanyadan Policy?